Portfolio managers' commentary

A review of Q4 2022

2022 year in review

Summary

- All ATB Investment Management funds (the funds) saw negative overall performance for 2022, although Q4 returns were positive for all funds. For the full year, total returns for the six Compass Portfolios ranged from -9.3% to -12.7%, and the four ATBIS Pools ranged from -4.5% to -14.7%.1

- 2022 was a particularly difficult year for investors, as both equity and fixed-income markets experienced double digit losses. Canadian bonds overall fell by 11.7%—the worst calendar-year performance since 1957.

- Canadian investors benefited from stronger foreign currencies over the last quarter boosting overseas equity returns in CAD terms, and from significant outperformance in energy stocks.

ECONOMICS

The global economy drove much of the market volatility experienced during 2022. Elevated inflation during the second half of 2021 was considered transitory, but as prices kept going up during the first half of 2022, central banks raised interest rates to counter, with hikes of up to 1% at a time, as we saw in Canada. Parts of the economy remained strong, however, especially employment and consumption, which hampered efforts to cool demand. Contrarian investor behaviour, such as “positive” economic data often leading to negative market performance, was common as 2022 wound down.

Geopolitically, Russia’s invasion of Ukraine also caused economic stress, leading to commodity price spikes and general uncertainty. The conflict also raised questions surrounding China’s ambitions towards Taiwan. An invasion of the island nation would certainly trigger more economic uncertainty and market volatility given the volume of both countries’ exports.

Going forward, 2023 expectations are for economic growth to be muted, and possibly negative in some advanced European economies.2 Recession chatter is increasing, but there has been little evidence that any major economy has fallen into recession. With inflation falling the past few months, there is hope that rate hikes will slow, and markets will normalize.

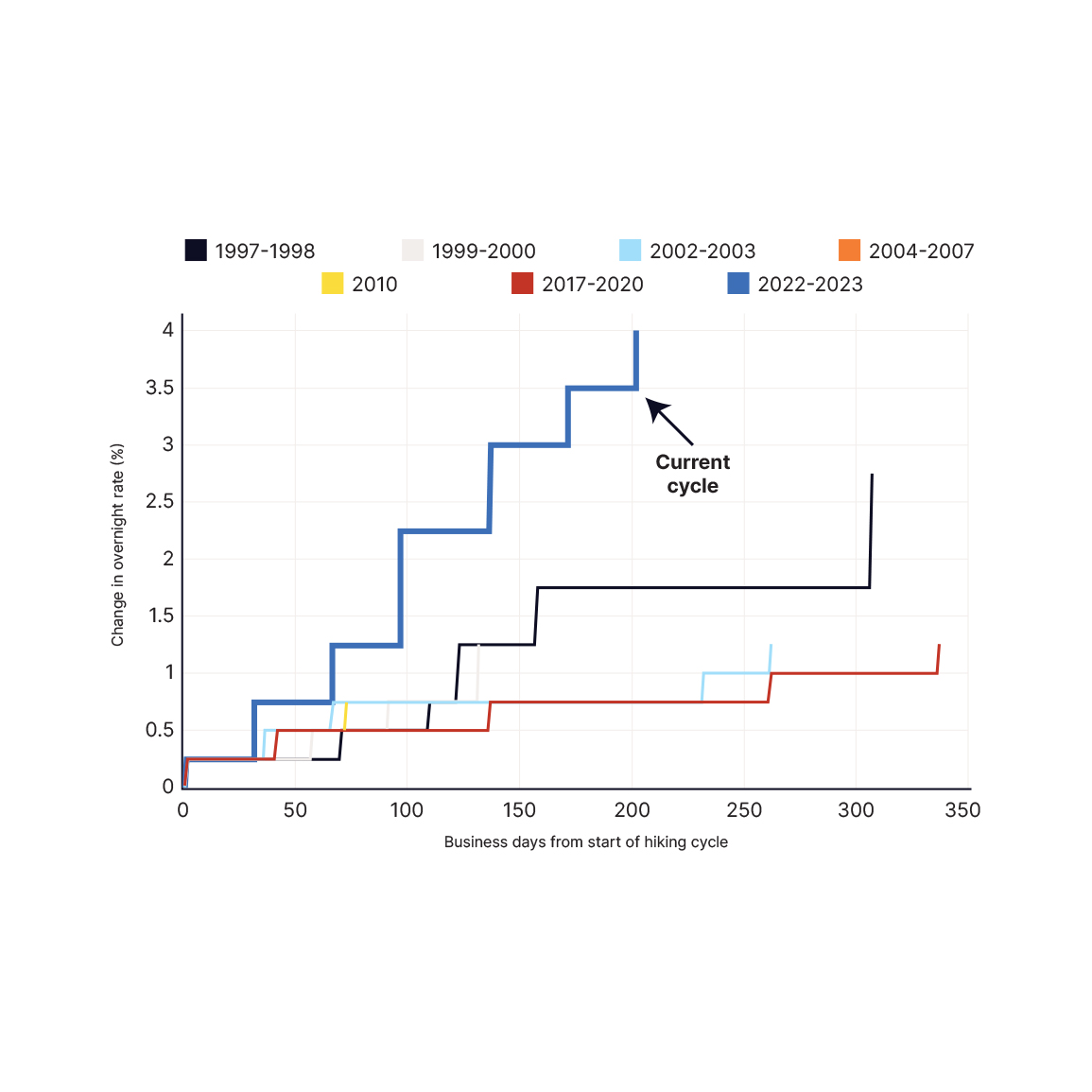

FIXED-INCOME MARKETS

This was, without a doubt, an outlier year for fixed income. As shown in the chart, the constant and higher-than-expected rate hikes to combat inflation pushed up the Bank of Canada’s (BoC) target for the overnight rate at a pace not seen for decades.

Fastest increase since the BoC started using the target for the overnight rate in 1994

Source: Bank of Canada via Bloomberg

Bond prices, being inversely related to yields, declined in lockstep. What happened in the first half, however, did not mirror the second half. The Bank of Canada raised its short-term target rate through the last six months of the year from 1.5% to 4.25%. Despite the short-term target rate rising 2.75% over that period, the average bond in Canada only moved up about 0.4% peaking in October. Central banks may still be on the path of hiking, but likely at a reduced pace as most are expected to reach their terminal (peak rates) by mid-2023. It’s a strong reminder that markets are forward looking. Mid- and longer-maturity bond yields didn’t rise as much in the latter half of the year, reflecting lower future rate expectations. The last two quarters may not feel like it, but both generated positive returns for fixed-income investors as a result.

Within the funds, the fixed-income holdings for the year declined by about 8.5% compared to the average bond in Canada down 11.7%. Holding bonds that were shorter in term, and therefore less price sensitive to interest rate movements, was the primary difference. The last quarter also saw positive relative returns with the fund's fixed income gaining roughly 1% compared to 0.6% for the FTSE Canada Universe Index—shorter-term holdings again contributing to the difference while seeing less volatility as well.

The changes we made in the fixed-income portfolios in 2022 centred around building quality. While the central banks don’t intend to cause recessions with rate hikes, it’s a higher possibility. Should that happen, higher-quality bond holdings such as government-backed bonds tend to preserve value while also maintaining excellent liquidity. Prices may fall in lower-rated issues coinciding with recessionary fear. This in turn can create opportunities for those that have higher-quality bonds to sell and deploy should lower-rated bonds represent attractive values. Because of the changes we made to fixed income, holdings with high quality AA and AAA ratings increased from about 27% to 42%, back to our position at the end of 2019. The vast majority of this quality change came from our sub-advisor Canso adding to Canadian federally backed positions. The increase was also supported by non-rated individual commercial mortgages being securitized into tradable rated securities in December, averaging an AA rating.

No one knows for sure if credit markets will worsen next year. If they do, the funds will be capable of being opportunistic as they were in 2020 when the COVID-19 recession materialized. In the meantime, carried yields are far higher than they were at the end of 2021 with the average bond held in the funds priced to roughly a 6% yield-to-maturity at year-end.

Broad equity and Canadian bond total returns (all in CDN terms) - 2022

Source: Bloomberg

EQUITY MARKETS

Equity markets also saw weakness in the face of aggressive central bank policy and uncertainty from the invasion of Ukraine, and China’s COVID-19 policies. European stocks in particular underperformed as soaring energy costs added to the uncertainty caused by the war. Making matters worse for investors was market reaction to economic news. What was once perceived as good news resulted in markets falling, whereas poor economic news was seen as a positive for markets–all due to the anticipated reaction from central banks. For example, following the release of strong or positive economic data, the expectation is that central banks looking to curb inflation through slower economic growth would react by restricting monetary policy further, heightening the chance of overtightening, and likely prolonging any eventual slowdown.

Over the year there was moderate movement within equity names across all the active mandates. The funds saw roughly 40 new companies added and just over 50 positions exited. Active equity positions tend to be around 250 to 300 companies (active does not include those held in passive indexed exchange-traded funds and pools), so on the surface there were quite a few companies turning over. Most of that turnover, however, was in companies with lower weights in the portfolios. On a weighted basis, about 10%3 of the equity portion within each fund was changed through the year. Themes for changes—other than the more typical valuation, or other material company changes—mostly centred around companies that may be hindered or benefit from excess inflation or various recent geopolitical events. The vast majority of the holdings remained the same with sub-advisors focused on finding well-managed resilient businesses capable of thriving through both good and bad economic environments.

Combined equity performance within the funds ended close to overall benchmarks4 with Canada and the US both ahead of broad benchmarks, but international lagging. For international, this could be attributed to the additional small- and mid-cap exposure that historically has added value in overseas developed markets, but lagged this year.

In early December, Picton Mahoney Asset Management (Picton) was added as a new Canadian equity small-cap sub-advisor for the funds. Picton was selected for its attractive risk-adjusted performance, and consistent downside protection compared to similar managers while complementing the existing Canadian equity sub-advisors from a diversification standpoint. All Compass Portfolios besides the Compass Conservative Portfolio were given an allocation to Picton, as well as the ATBIS Canadian Equity Pool.

Compass Portfolios returns - Series A

Total returns

Source: ATBIM

ATBIS Pools returns - Series F1

Total returns

Source: ATBIM

CLOSING REMARKS

2022 was a challenging year for financial markets. The uncertainty surrounding high inflation, interest rates and the Russia-Ukraine conflict all contributed to negative performance for both equities and bonds. As inflation moderates, however, it remains important to stay invested. Occasional volatility will likely continue, but we remain confident that the strength of our portfolios will help mitigate the short-term impact of volatility and achieve our portfolio investment objectives over the long run.

1 Compass Portfolio Total Returns for series A, and ATBIS FI Pool Total Returns for series F1

2 International Monetary Fund World Economic Outlook Report, October 2022

3 Not including trading turnover from general rebalancing and fund flows

4 S&P TSX Composite TR Index for Canadian equities, S&P 500 TR CAD Index for US equities, and MSCI EAFE Net TR Index for international equities.

This report has been prepared by ATB Investment Management Inc. (ATBIM). ATBIM is registered as a Portfolio Manager across various Canadian securities commissions with the Alberta Securities Commission (ASC) being its principal regulator. ATBIM is also registered as an Investment Fund Manager who manages the ATB Funds, Compass Portfolios and the ATBIS Pools. ATBIM is a wholly owned subsidiary of ATB Financial and is a licensed user of the registered trademark ATB Wealth.

The performance data provided assumes reinvestment of distributions only and does not take into account sales, redemption, distribution or optional charges or income taxes payable by any security holder that may reduce returns. Unit values of mutual funds will fluctuate and past performance may not be repeated.

Mutual Funds are not insured by the Canada Deposit Insurance Corporation, nor guaranteed by ATBIM, ATB Securities Inc. (ATBSI), ATB Financial, the province of Alberta, any other government or any government agency. Commissions, trailing commissions, management fees, and expenses may all be associated with mutual fund investments. Read the fund offering documents provided before investing. The ATB Funds, Compass Portfolios, and ATBIS Pools include investments in other mutual funds. Information on these mutual funds, including the prospectus, is available on the internet at www.sedarplus.ca.

Past performance is not indicative of future results. Opinions, estimates, and projections contained herein are subject to change without notice and ATBIM does not undertake to provide updated information should a change occur. This information has been compiled or arrived at from sources believed reliable but no representation or warranty, expressed or implied, is made as to their accuracy or completeness. ATB Financial, ATBIM and ATBSI do not accept any liability whatsoever for any losses arising from the use of this report or its contents.

This report is not, and should not be construed as an offer to sell or a solicitation of an offer to buy any investment. This report may not be reproduced in whole or in part; referred to in any manner whatsoever; nor may the information, opinions, and conclusions contained herein be referred to without the prior written consent of ATBIM.